Birthday Rule for Senior Citizens and Very Senior Citizens under Income Tax Act

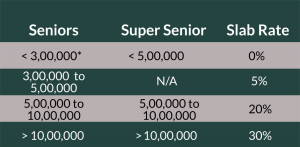

Income upto Rs. 3,00,000/- is exempted under Income Tax Act for Resident Senior Citizens.

Similarly, Income upto Rs. 5,00,000/- is not taxable for Resident Very (Super) Senior Citizen.

Individual,who is of the age of 60 years or more, but less than 80 years at any time during the previous year/financial year is Senior Citizen.

In the same line, Individual, who is of the age of 80 years or more, at any time during the previous year/financial year is very/super Senior Citizen.

For example:

Suppose today is January 01, 2020), the previous year/ financial year is 2019-20 (assessment year will be 2020-21)[assessment year is always following the previous year]. If an individual's 60th birthday falls in any time during financial year 2019-20, his income upto Rs. 3,00,000/- is exempted from Income Tax.

Similarly, If any individual has celebrated his 80th birthday, any time during the previous year 2019-20, the income tax rate is relaxed rate (upto Rs. 5,00,000/-).

If 60th or 80th birthday falls on 1 April. what will happen?

because, from 1st April, one previous years/financial year ended and next previous year/financial year starts.

For example:

In previous year/financial year 2019-20 (from 1st April 2019 to 31st March 2020).

Mr. A's birthday was in 2nd April 2019 - He is Senior Citizen for Income of previous year/financial year 2019-20.

(Rule - Individual,who is of the age of 60 years or more, but less than 80 years at any time during the previous year/financial year is Senior Citizen)

But, if Mr. A's birthday falls on 1st April 2020 - Should Mr. A is eligible for Senior Citizen's benefits in previous year 2019-20? (whereas previous year 2019-20 has ended on 31st March 2020 - and not on 1st April 2020)

Income Tax Act provided clarification regarding attaining the age of 60/80 year, for individuals, whose birthday fall on 1st April every year.A person born on 1st April would be considered to have attained a particular age on 31st March, the day previous the anniversary of his birthday.

Hence, in the above case, Mr. A would be eligible for getting the benefits of Senior Citizen in the previous year 2019-20 itself.

Therefore, a resident individual whose 60th/80th birthday fall on 1st April 2020, would be treated as having attained the age of 60/80 years in the previous year 2019-20, and would be eligible for higher basic exemption limit of Income Tax of Rs. 3,00,000/- and Rs. 5,00,000/- respectively, in computing the tax liability for previous year/financial year 2019-20 (assessment year 2020-21).

@FinanceSikho